Credit scores, those numbers that range from 300 to 850, are important. If your score is above 750, you rarely hear “no” when you apply for a loan and your interest rates are the lowest possible on the market. Have a credit score below 650 and you pay more interest on the money you borrow – if you’re even allowed to borrow at all.

No matter how good or bad your credit score is, there is always room for improvement. And there are tactics that will help you improve it. Unfortunately, there are no quick fixes, and people who tell you otherwise are usually looking to charge you a fee for the often nefarious “credit repair services.”

Time and discipline are the keys to repairing your credit. The third key is this guide, which outlines tried-and-true steps that you can take to repair and increase your credit score.

Looking to buy a home? Check out BEX Realty to search real estate listings, find condos and homes for sale, and work with their unequalled realtors and concierge service throughout the home buying process.

Read Your Credit Report – Carefully

Before you do anything, you should request a copy of your credit report from the three major credit reporting agencies and read it carefully. You’re entitled to one free credit report per year from each of three bureaus.

Credit reporting bureaus are known for making mistakes, so check your report for errors and immediately report it to the offending credit bureau. They have 30 days to investigate the error and respond to your inquiry.

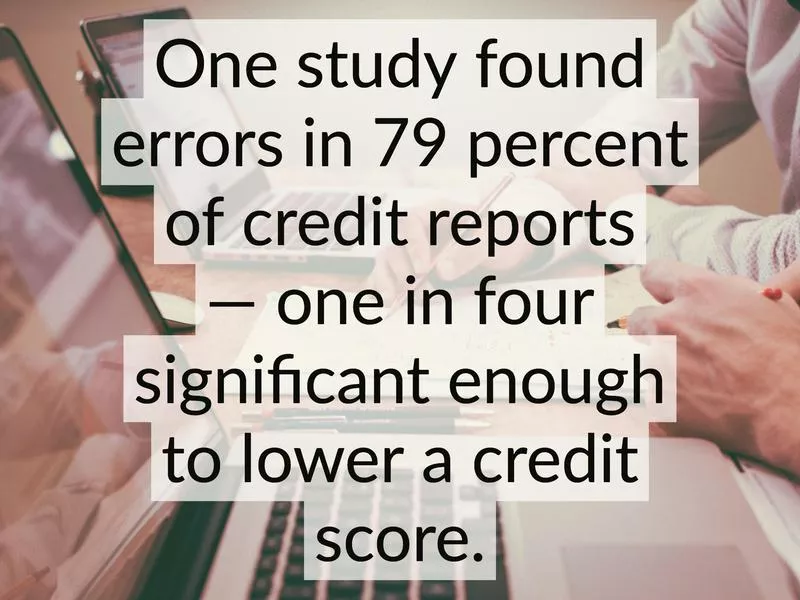

Mistakes happen often. One study found errors in 79 percent of credit reports, with one in four of those errors being significant enough to lower a credit score. They also happen for a variety of reasons. The credit bureau, for example, may put information from someone with a similar name on your report. Make sure you check for accounts you have never opened, addresses you have never lived at, a wrong date of birth or Social Security number and an inaccurate reporting of delinquencies.

Pay Your Bill On Time

Maybe we’re stating the obvious, but the truth is there’s no better fix to a sloppy credit score than time. A track record of paying your bills on time is the biggest factor taken into account when your credit score is calculated, and a late payment can do far more damage than anything you can do to boost your score to balance it out.

If you think you’re going to be late on a payment, call the creditor before the due date passes and explain the situation. They may have a one-time late payment forgiveness program, or they may be able forgo reporting the payment to credit monitoring agencies. They’ll usually ask you when you can make the payment by, and its important you make the payment before the agreed upon revised due date.

CreditCardInsider.com Founder John Ganotis urges people to set up automatic payments through their bank account so they don’t fall behind and have their report dinged with a late payment.

“If you’re serious about maintaining and maximizing your credit scores, the biggest thing you’ll want to do is make sure you pay all your bills on time,” he said. “If you make a late payment or let an account to go to collections, that negative item on your credit reports will usually hold your credit scores down for years.”

Understand How Credit Utilization Works

Companies use your payment history to calculate 35 percent of your credit score. Almost as important is your credit utilization, which accounts for 30 percent of your credit score and measures how much of your available credit you use.

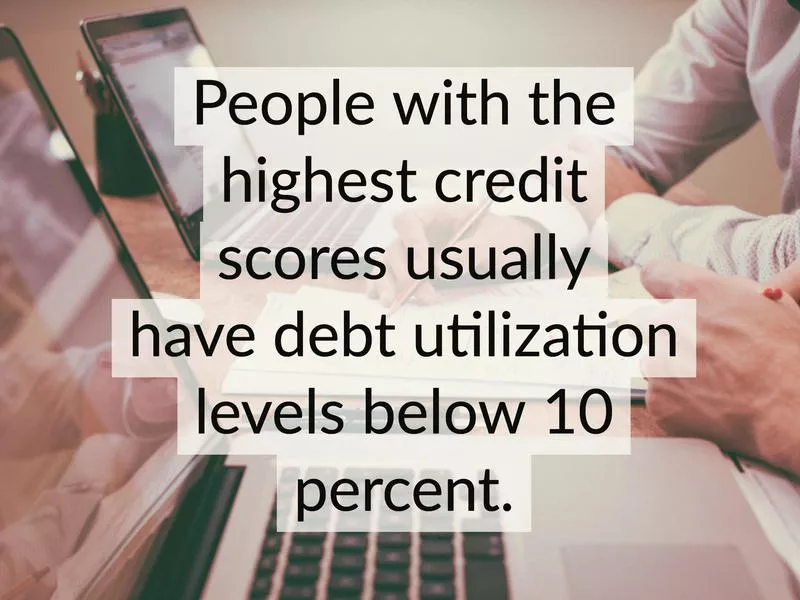

Creditors generally want to see you keep credit usage under 30 percent. In other words, if you have a credit line of $1,000, you don’t want to use more than $300 of it. And people with the highest credit scores usually have debt utilization levels below 10 percent. Experts warn to never let your total credit usage rise above 50 percent unless you want your credit score to take a dramatic drop.

Keep in mind this portion of your credit score doesn’t measure your total debt, but the percentage of debt you are using. If you have $250 on four credit cards with credit limits of $1,000 each, you may think transferring all of the balances to a single card and closing the other three accounts is a sound financial move. But in reality, you’ve gone from using 25 percent of your available credit to 100 percent of your available credit, which will negatively impact your credit score even though you have not increased your total amount of debt.

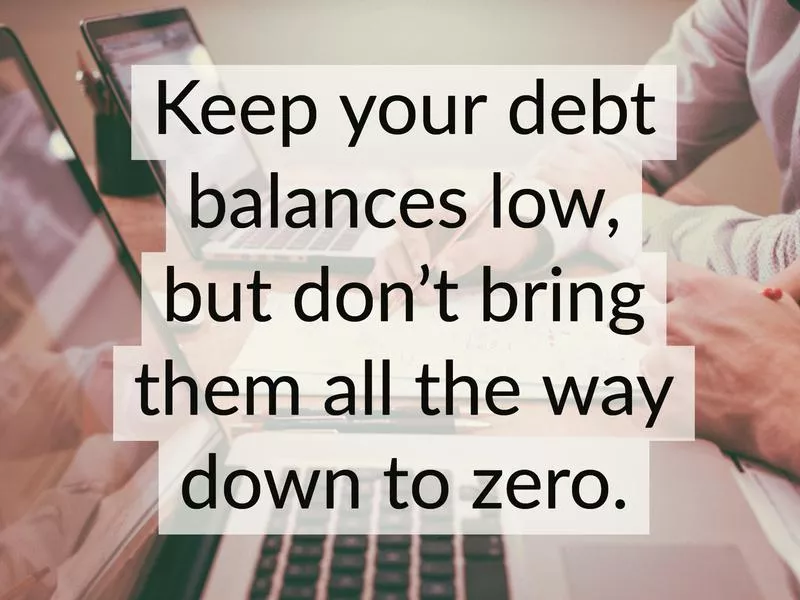

One more word of caution. While a low percentage of credit utilization is ideal, you can actually go too low, Ganotis said. “Generally, the closer your utilization is to 1 percent the better it is for your credit scores, as long as it’s not 0 percent,” he said.

Use Your Credit Card Like a Debit Card

So you want to keep your debt balances low, but not bring them all the way down to zero. One obvious problem with that is that balances on credit cards get charged interest unless you pay them off every single month.

Natasha Rachel Smith, a personal finance expert at TopCashback.com in Montclair, N.J. recommends using your credit card the way you’d use a debit card tied to your checking account.

“One of the best ways to get your credit score up is by making all your purchases on your credit card but never exceeding how much you have on your debit card,” she said. “The reason being … you can repay any debt you accumulated through your credit card without accruing any unnecessary interest and keeping your credit utilization ratio low.”

Added bonus: If your card rewards you with points or frequent flier miles, you’ll accumulate those points without accumulating interest.

Open a New Credit Card Account

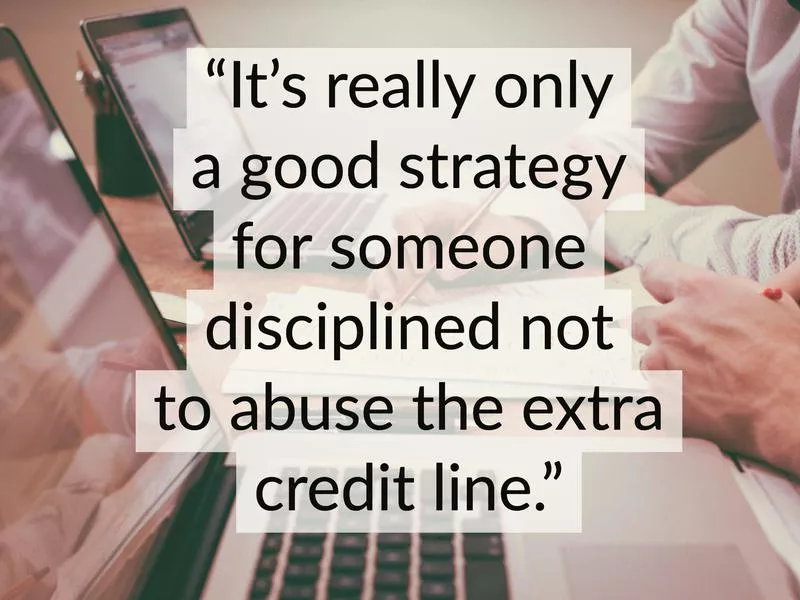

When Lou Haverty of the FirtClassTravelGuide.com wanted to boost his credit score he did something that may seem counterintuitive: he opened new credit card accounts and made sure that he never used them. The reason his gambit worked is because, after on-time repayment history, the biggest factor used to calculate your credit score is something called credit utilization.

Credit scoring companies like to see that even though you could max out your credit cards, you don’t do that. Using 30 percent or less of your credit is the standard you should shoot for; in other words, if you have a credit limit of $1,000, you should never have a balance of more than $300. The most obvious way to reach a favorable credit utilization level is to pay down the balance to get under the 30 percent threshold. But increasing your credit limit effectively does the same thing.

“If you have a low credit utilization score, that will have shortest term improvement in your score as long as you don’t miss a payment or do something that offsets the benefit from a low utilization ratio,” Haverty said. “I’ve seen it first hand with the improvement in my own score when I’ve opened new credit cards over the last year. The problem is that it’s really only a good strategy for someone disciplined not to abuse the extra credit line.”

Pay Your Credit Card Bill More Than Once a Month

Your credit score won’t be hurt if you make more than just a single monthly payment. There are two advantages to this. First, it helps you avoid those late payments that are so damaging to your credit score. But it also helps you keep your credit utilization above the dreaded 0 percent without accumulating interest on balances, according to Smith, the personal finance expert who recommends using your credit card like a debit card.

“You can avoid paying high interest on your credit card purchases by paying down debt as soon as possible. If you’re able to get in the habit of repaying the balance each week, this is a strong and almost-secret trick to improve your credit score,” Smith said.

You Don’t Need to Marry Rich, But Marry Someone With a Great Credit Score

No, we’re not really suggesting you make a marriage decision based on money, but if your spouse or someone else you trust has a great credit score and is willing to make you an authorized user on one of their accounts, you should see a significant bump in your credit score.

“There aren’t many shortcuts in credit building, but this is one of them. If someone you trust has a well-maintained card that has a long, flawless payment history, they can help you out big-time by adding you to that account as an authorized user,” said Carson Yarbrough, a personal finance specialist with Offers.com. “Once you’re added, that account will show up on your credit reports. And as long as the account remains in good standing, you (and your score) will get credit for it as the data from your credit reports feeds into your credit score.”

Know ALL of Your Credit Scores

Too many people think they have just one credit score. In reality, you have a score at each of the main credit reporting bureaus – and how prospective lenders use those scores can vary depending on the time of loan you’re applying for. For this reason, it’s smart to review and track multiple components of your overall credit ‘report card’.

“I talk to many people who mistakenly think they only have one credit score, when one person can actually have dozens of different credit scores. Even under the FICO brand there are several different models used for different purposes, like for considering a mortgage application versus a credit card application,” Ganotis said. “Also, each score can be calculated using information from one of your three credit reports. Since information can vary from one credit report to the next, the same type of score calculated from each can vary, too.”

Don’t Close Credit Card Accounts Once They’re Paid Off

A lot of people trying to boost their debt score make the mistake of closing a credit card account once its paid off. Their rationale is that, once the account is closed, they won’t be tempted to use it and wrack up a fresh round of credit card debt. But closing accounts can damage your credit score, according to Smith.

That’s because credit agencies qualify borrowers as being a responsible customer depending on how much of their credit access is available, so exceeding more than 30 percent at any point in a billing cycle could damage their credit score.

“While it is tempting to say goodbye to a card forever, it’s in your best interest to keep it,” Smith said. “I also recommend keeping the credit card you’ve held the longest to minimize any additional damage to your credit score since the length of holding a credit item plays a role in credit scoring as well. The longer your relationship with a provider, the better you’re viewed.”

Get a Credit Builder Loan

These types of loans are usually offered by credit unions. The principal of the loan is secured by money that you put into an account at the credit union, and you can’t access that account until the loan is paid off. The loans typically have short repayment times of six to 12 months, and payments are reported to all three credit bureaus.

If you don’t qualify for credit union membership, you can often access secured credit card counts that act in the same way.

Discover It, for example, offers users a card that is accepted anywhere Discover is accepted. But the credit line of the card is secured by a deposit you make. After eight on-time payments, Discover sends your deposit back and changes your account to an unsecured card.

Looking to buy a home? Check out BEX Realty to search real estate listings, find condos and homes for sale, and work with their unequalled realtors and concierge service throughout the home buying process.