The Most Important Financial Goals to Achieve Before Turning 40

Your thirties are a turning point. Careers settle into shape, families often begin to grow, and the choices you make with money start to carry real weight. By the time you reach 40, your finances should give you stability in a crisis and room to plan for the future. It isn’t about penny-pinching or chasing risky investments. What matters most are the habits and systems that keep your money working for you, so you can focus on the life you want to live.

Pay Off All Non-Mortgage Debt

Credit: Getty Images

Debt is a drag on your entire financial life. Start by paying off high-interest credit cards, then move to car loans and personal loans. Use strategies like the debt snowball (paying the smallest balances first for motivation) or debt avalanche (tackling the highest interest rates first to save money). It feels like freedom when you’re getting your full paycheck without deductions for past decisions.

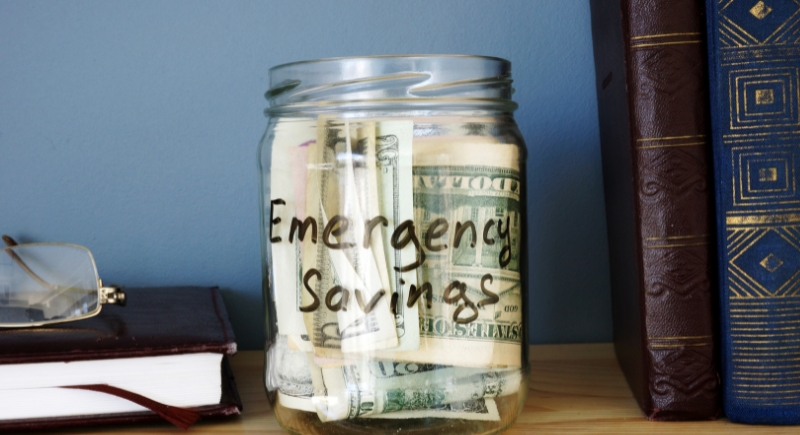

Build a Six-Month Emergency Fund

Credit: Getty Images

A job loss, medical emergency, or major home repair can wipe out savings. That’s why you need a dedicated emergency fund with 6 months of essential expenses. But if you have children, own a business, or work in a volatile industry, aim for 9 to 12 months. Keep this fund in a high-yield savings account for the best results.

Review and Improve Your Credit Score

Credit: Getty Images

A strong credit score opens doors to better loan terms, lower interest rates, and easier approval for housing or business financing. By 40, aim to keep your credit utilization below 30%, pay on time, and regularly check your credit reports for errors. Good credit saves money across your entire financial life.

Increase Your Main Income

Credit: Canva

Your primary paycheck is the engine that powers every financial goal. Don’t wait for someone else to recognize your value. Invest in yourself by earning certifications or even switching industries. A $10,000 raise today compounds over time into thousands more in lifetime earnings.

Create Additional Income Streams

Credit: Getty Images

Side hustles create stability and flexibility. Start with something that leverages your skills or passions. It could be freelance writing, photography, tutoring, consulting, or even selling products online. Even if you never quit your main job, having multiple streams of income gives you choices and reduces the fear of sudden job loss.

Max Out Retirement Contributions

Credit: Getty Images

Retirement accounts like 401(k)s, IRAs, and Roth IRAs are tax-advantaged growth machines. When you contribute, you create a snowball effect where your money earns returns, and those returns earn even more returns. Even small, consistent contributions now mean you won’t have to scramble in your fifties to catch up.

Use Employer Matches

Credit: Getty Images

An employer match is usually a 50% to 100% return on your money. If your company offers to match contributions up to a certain percentage, make sure you at least contribute enough to get the full match. Otherwise, you’re just leaving free money on the table.

Raise Contributions Gradually

Credit: pexels

It is unrealistic to think that you can go from contributing 5% of your income to 20% overnight. Instead, promise yourself to increase contributions by a certain percentage every time you get a raise or a bonus.

Invest Outside Retirement Accounts

Credit: Canva

Retirement accounts are powerful, but they have restrictions and penalties for early withdrawal. If you plan to achieve big goals, like buying a house or starting a business, your investments need to be more flexible. A taxable brokerage account gives you liquidity.

Treat Brokerage Accounts as Growth Tools

Credit: Getty Images

Stick to low-cost, diversified index funds or ETFs to reduce risk. And then, be patient. Let compounding work in the background, and don’t raid the account unless it directly aligns with your long-term vision. Make sure every dollar you put in there has a purpose.

Update Beneficiaries Regularly

Credit: Getty Images

The people you want to leave your assets to at 25 may not be the same at 40. Marriage, divorce, or children can all change those priorities. If the paperwork isn’t kept up to date, your money could end up in the wrong hands or tied up in court. A quick review every few years avoids problems later.

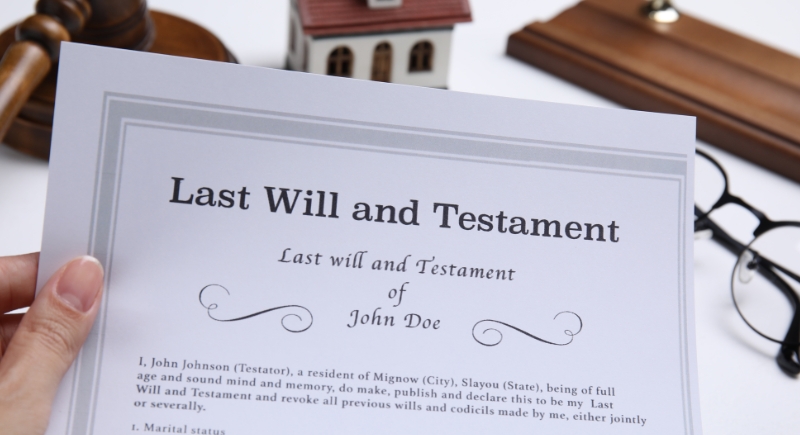

Create a Will

Credit: Africa Images

If you don’t have a will, the state decides where your money and property go—and who cares for your children. That process can be slow, costly, and stressful for your family. A basic will spares them that burden and makes sure your wishes are clear.

Organize Important Documents

Credit: pexels

The last thing you want is to be hunting for insurance papers or account numbers in times of crisis. Gather bank accounts, deeds, tax returns, and passwords into one secure location. Digital solutions like encrypted password managers or secure cloud storage make this easy. Share access with one trusted person so they can step in if you’re unable to manage things yourself.

Review Estate Plans Annually

Credit: Canva

Set a yearly reminder to review wills, trusts, beneficiaries, etc., and ensure they are in line with your current priorities. This keeps your legacy aligned with your values and prevents unpleasant surprises. Your estate plan should evolve with your life.

Protect Your Health

Credit: Getty Images

Being healthy is a sound financial decision. Preventive care is cheaper than treatment, so don’t skip annual checkups, dental visits, and screenings. Prioritize exercise, sleep, and stress management. They’re free and have massive long-term payoffs. Also, consider disability insurance.

Set Work-Life Boundaries

Credit: Getty Images

Earning more is pointless if you burn out before you can enjoy it. So while you work hard, take some time out for yourself as well. Set clear boundaries, like no work calls during family dinners or weekends reserved for rest. This keeps you sane and protects your energy and relationships.

Value Time Over Money

Credit: pixabay

Money comes and goes, but time does not. As your income grows, use it to reclaim hours for things that matter. Hire help for chores, pay someone to do the laundry for you, or move closer to work to cut down on commuting. This shift in mindset turns money into a tool that buys you freedom.

Start Investing Early

Credit: Getty Images

The sooner you put money into the market, the more time it has to grow. Even modest amounts invested in your 30s can turn into a meaningful nest egg by retirement. If you’re closer to 40 and just getting started, it’s still worth it. A few years of steady contributions can show real results.

Plan for Major Life Expenses

Credit: Canva

Financial stability means looking ahead. Will you help pay for a child’s college, care for aging parents, or buy a second property? Start building separate sinking funds for these large future costs. Planning early avoids financial strain later and helps you make confident decisions when those moments arrive.

Invest in Career Growth

Credit: Getty Images

Your skills are your greatest asset. Technology evolves, and job markets shift, and you need to keep up if you want to continue earning. Investing in certifications, degrees, or portfolio projects keeps you competitive. It also gives you leverage in salary negotiations and opens doors to higher-paying roles.